Contents

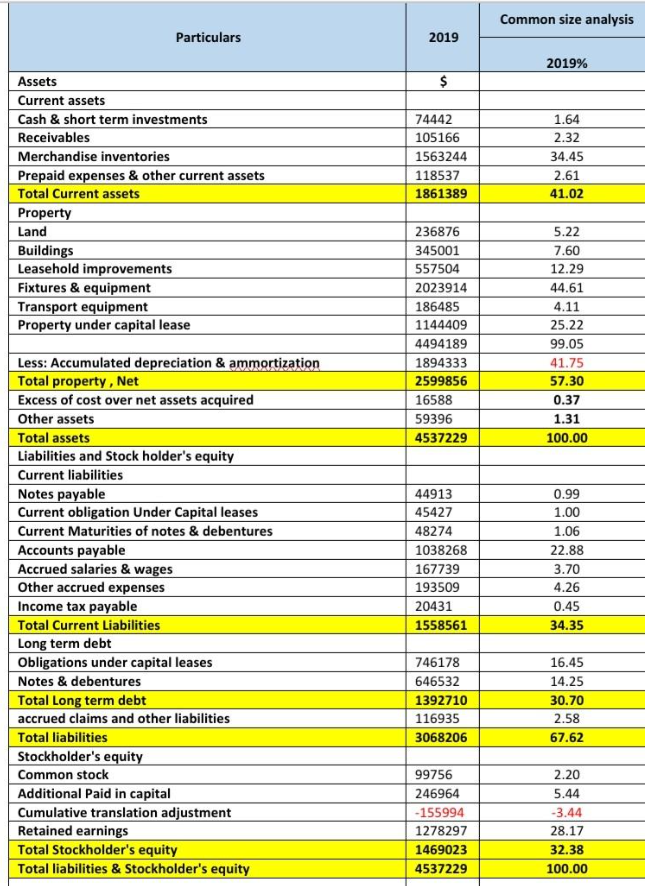

detailed balance sheet for a hypothetical cement factory

TO Download this post and all the books and excel sheets and my personal notes and presentations I collected about cement industry in the last 30 years click the below paypal link

Creating a detailed balance sheet for a cement factory requires making realistic assumptions about the financial figures. Below is an example of a detailed balance sheet for a hypothetical cement factory, including common line items you might find in such an industry. The figures provided are illustrative and based on industry averages and estimated data.

ABC Cement Factory

Balance Sheet As of December 31, 2023

Assets

- Current Assets

- Cash and Cash Equivalents: $15,000,000

- Accounts Receivable: $20,000,000

- Inventory:

- Raw Materials: $8,000,000

- Work-in-Progress: $5,000,000

- Finished Goods: $12,000,000

- Spare Parts & Consumables: $4,000,000

- Prepaid Expenses: $1,500,000

- Other Current Assets: $2,500,000

Total Current Assets: $68,000,000

- Non-Current Assets

- Property, Plant, and Equipment (PPE):

- Land: $30,000,000

- Buildings: $50,000,000

- Plant & Machinery: $200,000,000

- Vehicles: $10,000,000

- Office Equipment: $3,000,000

- Accumulated Depreciation: -$50,000,000

- Intangible Assets:

- Goodwill: $5,000,000

- Patents & Trademarks: $2,000,000

- Investments in Subsidiaries/Affiliates: $8,000,000

- Long-Term Investments: $7,000,000

- Deferred Tax Assets: $4,000,000

- Other Non-Current Assets: $2,000,000

Total Non-Current Assets: $271,000,000

- Property, Plant, and Equipment (PPE):

Total Assets: $339,000,000

Liabilities and Equity

- Current Liabilities

- Accounts Payable: $25,000,000

- Short-Term Debt: $10,000,000

- Current Portion of Long-Term Debt: $7,000,000

- Accrued Liabilities: $3,500,000

- Taxes Payable: $2,000,000

- Other Current Liabilities: $1,500,000

Total Current Liabilities: $49,000,000

- Non-Current Liabilities

- Long-Term Debt: $100,000,000

- Deferred Tax Liabilities: $5,000,000

- Provision for Environmental Liabilities: $3,000,000

- Pension and Post-Retirement Obligations: $4,000,000

- Other Non-Current Liabilities: $2,000,000

Total Non-Current Liabilities: $114,000,000

Total Liabilities: $163,000,000

- Equity

- Share Capital: $50,000,000

- Retained Earnings: $100,000,000

- Other Reserves: $20,000,000

- Non-Controlling Interest: $6,000,000

Total Equity: $176,000,000

Total Liabilities and Equity: $339,000,000

Additional Notes:

- Cash and Cash Equivalents include readily available funds and highly liquid investments with a maturity of three months or less.

- Accounts Receivable represent amounts owed by customers for cement and other products sold on credit.

- Inventory includes the cost of raw materials like limestone, gypsum, and other additives; work-in-progress for partially completed cement; and finished goods ready for sale.

- Property, Plant, and Equipment (PPE) are the most significant assets, including the cement plant, machinery, and other infrastructure essential for production.

- Goodwill reflects the premium paid over the fair value of assets when acquiring other businesses.

- Long-Term Debt mainly consists of bank loans and bonds issued to finance plant operations and expansion.

- Deferred Tax Liabilities arise due to differences in accounting and tax depreciation.

- Equity represents the owners’ investment in the business plus retained earnings from profitable operations.

This balance sheet gives a comprehensive view of a cement factory’s financial position, helping stakeholders understand its assets, liabilities, and equity at a specific point in time.

TO Download this post and all the books and excel sheets and my personal notes and presentations I collected about cement industry in the last 30 years click the below paypal link